Global listed infrastructure

Global listed infrastructure refers to publicly traded companies that own, operate, and/or develop infrastructure assets around the world. These public companies are listed on major global exchanges and provide mission critical infrastructure services such as transportation, utilities, renewables, energy storage, and communications.

Global listed infrastructure (GLI) equities offer investors liquid, daily-priced access to assets that are typically illiquid. As of December 31, 2025, the free float market capitalization of global listed infrastructure companies represented more than $3.3 trillion USD.

According to estimates provided by the Global Listed Infrastructure Organisation (GLIO), there is a global need for $94 trillion in investment in infrastructure by 2040, with an unmet investment gap of $15 trillion. After years of underinvestment, it is still early days for infrastructure investment, with catalysts such as global population growth, economic development, and technological advances supporting massive future demand. In addition, the definition of infrastructure is also evolving to match future needs, away from traditional asset-heavy definitions, to include services, technology, and distributed systems.

Asset obsolescence, expansive urbanization, and technological advancements have exposed the limitations of traditional definitions of physical infrastructure like roads, bridges, ports, and power grids. Today’s infrastructure assets now include hyperscaler data centers, fiber optic networks, logistic hubs, and energy renewables as essential underpinnings of modern innovation.

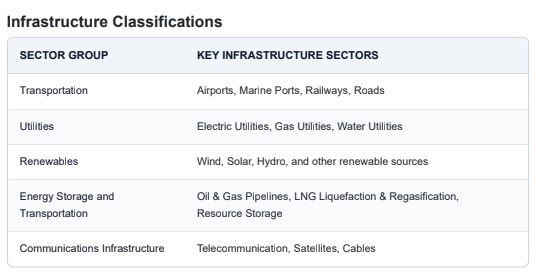

Infrastructure can be classified in the following sector groups and 11 key infrastructure sectors detailed in the graphic below:

Source: GLIO VettaFi

Over the past decade, private investment has played a pivotal role in infrastructure financing, with assets in private infrastructure funds tripling from $500 billion in 2016 to over $1.56 trillion, with a record $200 billion in private capital deployed in 2025. But private infrastructure investment alone will not meet the needs of the future, making global listed infrastructure even more critically important.

Global listed real assets

Global listed real assets refers to publicly traded securities backed by the underlying value of physical assets. Real assets derive their inherent value from their tangible, physical characteristics. Real assets can serve as stores of value and are fundamental to a functioning economy.

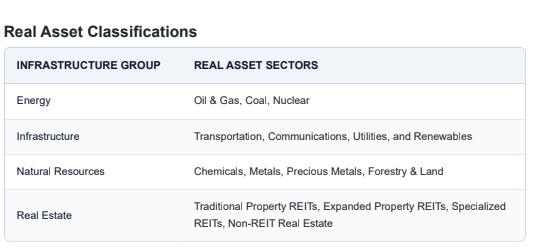

Global listed real assets can be separated into four infrastructure groups — energy, infrastructure, natural resources, and real estate — and the following real asset sectors detailed in the graphic below:

Source: GLIO VettaFi

Global listed real assets are assuming a more critical role within strategic allocations due to their innate ability to hedge inflation, enhance diversification, and provide income and yield generation, all in a liquid investment vehicle. Liquid real assets are attractive to individual and institutional investors seeking the benefits of tangible assets without the long-term, illiquid commitments of private investments. Additionally, in 2025, a supportive macro-economic environment, strong end-market demand, and attractive industry fundamentals provided further tailwinds for liquid real assets as an investment category.

The robust end-market demand for global listed real assets is being generated by many of the same secular growth drivers fueling demand for global listed infrastructure. The AI-driven surge in power demand is providing a meaningful boost to infrastructure, energy, and natural resource equities, including those with exposure to critical commodities such as copper, uranium, and natural gas. Rising demand, absent a commensurate rise in supply, is providing long-term support for real assets.

GLIO VettaFi Global Listed Infrastructure and Listed Real Assets Indices

VettaFi recently announced the acquisition of the Global Listed Infrastructure Organisation (GLIO) family of indices. The GLIO indices, known for their rigorous methodology and specialized focus on listed infrastructure and real assets, will be integrated into VettaFi's existing suite of indexes and rebranded as the following:

GLIO VettaFi Global Listed Infrastructure Index Series

GLIO VettaFi Global Real Assets Index Series

GLIO Founder and Chief Executive, Fraser Hughes, noted, "Our transition to VettaFi marks a key milestone in GLIO's evolution. By combining our listed infrastructure expertise with VettaFi's global platform, technology, and distribution, we are enhancing the visibility and accessibility of GLIO indices while strengthening the foundation for innovation, broader market access, and continued growth in listed infrastructure and real assets investment."

The acquisition marks another significant milestone in VettaFi's index benchmark and product capabilities which now also includes fixed income, derivative, and digital asset capabilities in addition to equities.

For more information about the GLIO VettaFi Listed Infrastructure and Listed Real Assets Indices, click here.