Fixed income ETFs now command trillions in assets and trade with equity-like immediacy. These wrappers let investors move in and out of diversified bond exposure in a single click, at a visible price, throughout the day. Yet beneath many of these modern products lies infrastructure designed for a different market era. Index methodologies conceived in the 1990s, built for a market that was traded by phone, settled by fax, and priced by educated guess. The wrapper has modernized, but the blueprint underneath has not.

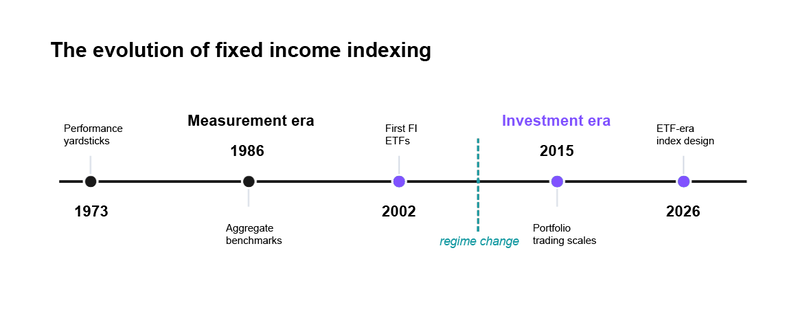

Fixed income benchmarks built for measurement, not investment

The first generation of bond indices was not designed to be traded. These were yardsticks for measuring manager performance in an over-the-counter market that was opaque, fragmented, and profoundly illiquid. Most bonds were rarely traded and prices were indicative at best. Replicating a broad index in an actual portfolio was, for practical purposes, impossible.

Index providers responded with sensible engineering for that era. They imposed liquidity screens and minimum issue sizes to keep indices anchored to bonds that could actually be found and traded. They sampled, selecting a subset of an issuer's bonds to stand in for its full debt structure, because holding everything was unrealistic. Each of these design choices was a rational answer to a genuine constraint. Liquidity was scarce and price discovery was scarcer.

ETFs changed how bond-market liquidity forms

The advent of ETFs and specifically trading via the creation/redemption mechanism changed how liquidity and price discovery function in bond markets. Every day, authorized participants assemble and disassemble baskets spanning thousands of individual bonds. Securities that once traded by appointment now print regularly as part of this continuous flow and electronic trading has only amplified this effect. The result is a market where tradability and price discovery — the scarce resources that legacy index rules were built to ration — have become abundant.

This is the paradox of today's fixed income index infrastructure. The liquidity screens, minimum balances, and sampling conventions that shaped legacy benchmarks still persist, even though the market conditions that justified them have long changed. It’s a classic example of a solution that has outlived its problem.

Full representation, not artificial sampling

As liquidity and price discovery improve, the design objective changes. A modern fixed income index should represent the market as it actually exists. That means representing an issuer's full debt structure, not only the curated subset selected by an index provider's sampling rules.

The distinction matters more than it may appear. When a provider samples, it is quietly making portfolio decisions on behalf of every investor tracking the index. Which bonds of an issuer count, and which do not. Full representation returns that decision to where it belongs. The index describes the complete opportunity set, and portfolio managers determine how to best represent a given issuer within their own funds, using their own tools — at their own transaction costs. The index provider defines the market. The portfolio manager implements it.

This shift reflects something larger. Index construction has become an engineering discipline rather than a purely mathematical one. The questions that matter today blend operational and market-structure capabilities. How does the index behave through rebalancing? How do the rules interact with real-world trading? How does the methodology hold up when markets are stressed rather than calm? The challenge is no longer simply to calculate the index, but to design benchmarks that reflect the structure of modern fixed income markets.

For investors, the benefit is not complexity for its own sake. It is a benchmark that better reflects the investable market, gives portfolio managers a cleaner opportunity set, and avoids embedding outdated implementation shortcuts into the index itself.

The upgrade is overdue

None of this is a criticism of the pioneers. Legacy benchmarks were well built to answer the constraints of their time. But those constraints have changed, and rules designed to solve yesterday’s problems can distort today’s portfolios.

The artifacts of that old era run deeper than what gets included in an index. There is a second legacy convention, hiding in plain sight, that shapes portfolios far more directly. Traditional benchmarks allocate weights based on total outstanding debt, which means that the more indebted an issuer becomes, the more of your portfolio it commands. Debt weighting is not an investment thesis.

Next time, we’ll examine why that is a bug, not a feature, and what to do about it.