Europe is undergoing an amazing industrial transformation with strategic plans for autonomy and self-sufficiency, aiming to reduce its dependency on non-European sources for critical areas such as:

- Defense and security

- Energy

- Infrastructure

- Supply chain

Defense and security

Global instability and increasing geopolitical competitiveness have accelerated Europe’s plans for defense autonomy and readiness. One prime example is the ReArm Europe/Readiness 2030 Plan, detailed in the graphic below, which includes €800 billion in defence-related investment to boost European defense capabilities and industry by the end of the decade.

The Russia-Ukraine War has been a wake-up call for Europe in terms of the need to invest more in defense equipment and modernization. The peace dividend era Europe enjoyed for so long has ended, and technology offers a more cost-effective path to achieving greater autonomy.

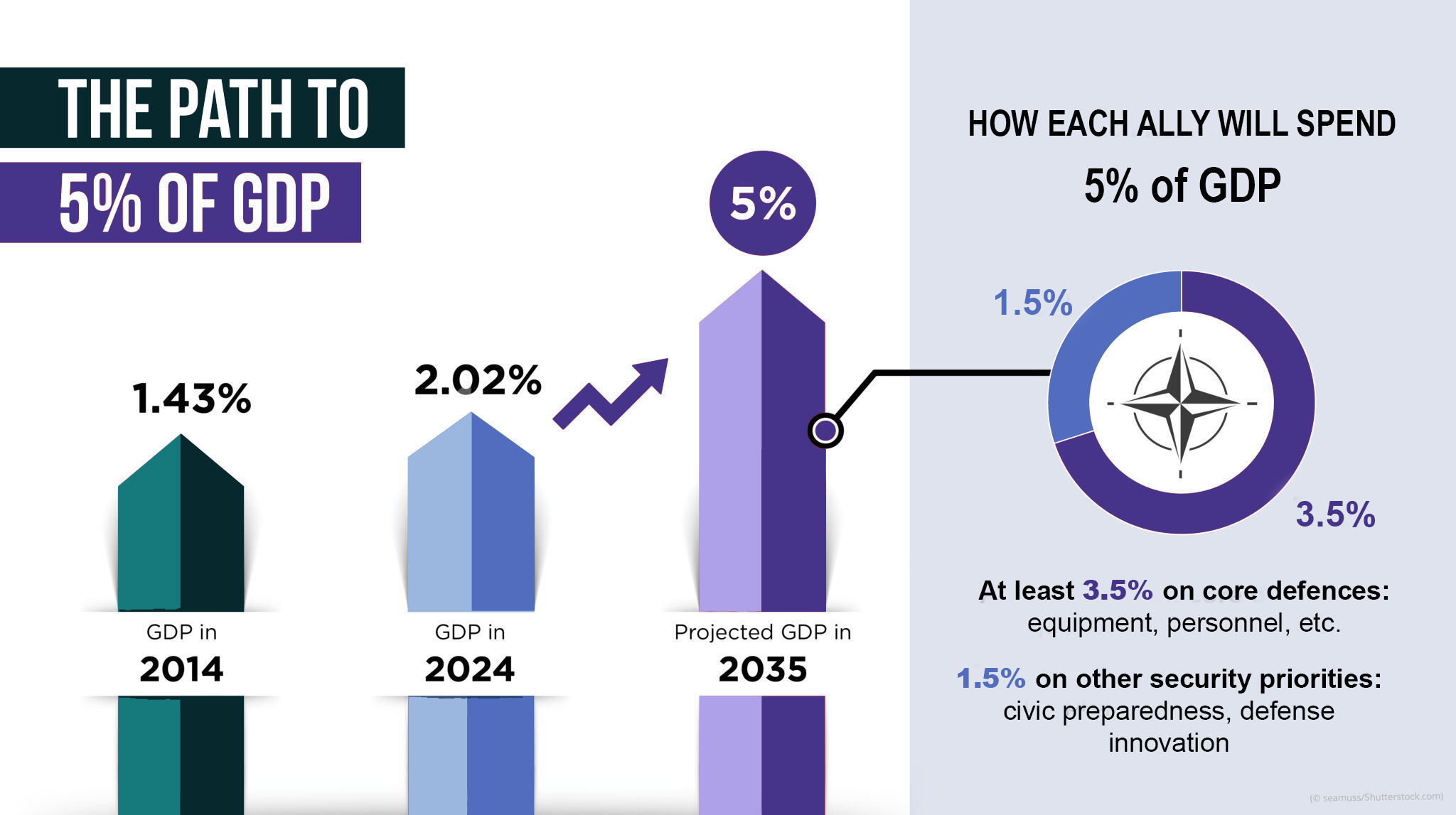

Another key driver of the boom in European defense spending has been NATO’s increased target for military spending, rising from 2% of GDP to NATO’s newly established 5% of GDP goal. The 5% goal includes a 3.5% allocation to traditional military expenditures with a 1.5% provision for cyber, defence technology, and infrastructure investments.

Source: ShareAmerica, US State Dept./H. Efrem

A key component of Europe’s plans is its European Defence Industrial Strategy (EDIS), focused on collaborative investment and coordination of defence capabilities, including initiatives like the Defence Industrial Preparedness Board and European Defence Projects of Common Interest. The European Sky Shield Initiative is a perfect example of Europe’s new defense industrial strategy, as a collaborative effort to create a European missile defence system that will include a space shield, air shield, eastern flank watch, and drone wall.

Energy security and independence

In addition to increased autonomy in defense, Europe is also pursuing a strategy for increased energy independence, reducing its reliance on Russia and boosting renewable energy and improved energy efficiency. REPower EU aims to make Europe independent from the import of Russian fossil fuels by the end of the decade. The European Commission has mobilized close to €300 billion to fund the REPower EU Plan. And earlier this year, Europe achieved an important strategic milestone with Baltic Energy Independence Day. Lithuania, Latvia, and Estonia have achieved full energy independence by building infrastructure like LNG terminals and synchronizing their energy systems with continental Europe, which has allowed them to cease trading with Russia and become energy independent as of February 8, 2025.

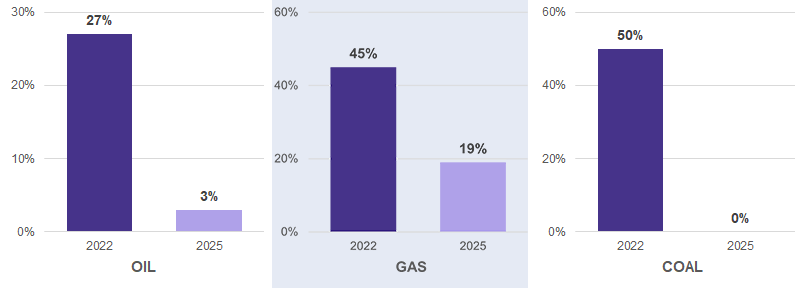

Prior to the Russia-Ukraine conflict, European energy imports from Russia were at a high level. However, now Europe is actively transitioning to other sources of energy.

- Coal - All imports of Russian coal are banned by EU sanctions.

- Natural gas - All imports of Russian pipeline and liquid natural gas (LNG) will terminate by the end of 2027.

- Oil - Actions have been taken to address Russia's ‘shadow fleet’ (vessels employed by Russia to evade sanctions) transporting oil and stop Russian oil imports by the end of 2027.

- Nuclear - Europe has restricted the import of uranium, enriched uranium and other nuclear materials coming from Russia. And EU countries still using Russian-designed pressurized water reactors are working to replace Russian nuclear fuel with fuel from other producers.

European energy imports from Russia

Source: European Commission

Closing the European infrastructure gap

European infrastructure investment is focused on closing a significant funding gap through a combination of public and private capital, prioritizing projects in sustainable transport, clean energy, and digital transformation. Europe has established several large-scale funding programs.

One of the largest programs is Germany’s government-approved €500 billion special fund, a 12-year plan to invest in infrastructure, climate protection, and modernization. Germany has extensive but aging infrastructure. This special fund is being deployed to improve railways, energy grids, and digital networks, alongside a focus on new technologies like hydrogen and geothermal energy. The plans are larger in scope than the Marshall Plan after World War II. Additionally, the historic levels of spending have required the relaxation of Germany’s constitutionally protected debt rules.

Other infrastructure plans in Europe include:

NextGenerationEU - A €750 billion stimulus plan designed to support a sustainable and resilient post-pandemic recovery, with a significant portion dedicated to green and digital transitions.

InvestEU programme - This program aims to mobilize over €372 billion in public and private investment using an EU budget guarantee of €26.2 billion.

Connecting Europe facility (CEF) - With a budget of over €33 billion, the CEF provides grants to co-fund TEN-T projects, with 60% of its budget allocated to sustainable infrastructure projects.

Cohesion policy funds - Funds aiming to reduce disparities between regions have financed nearly €300 billion of investments through grants in previous periods, supporting various infrastructure projects, especially in less developed regions of Europe.

Economic and supply chain resilience and re-industrialization

Europe is working to create a more resilient supply chain by increasing domestic capacity and reducing foreign dependence for key technologies and industries. Key efforts include:

- Resilient EU2030 – Spain’s proposal, which provides a roadmap to reinforce Europe's strategic autonomy and global leadership in sectors such as energy, digital technologies, health, and food.

- European economic security strategy – Addresses risks related to critical technologies and their supply chain. The European Commission has proposed measures to safeguard research activities and make international partnerships more selective, prioritizing those that align with EU values.

- Reshoring – “Smart reshoring" plans to redeploy industries to the EU, increase production and investment, and secure more strategic industries. Microsoft, Volvo, Sanofi, GSK, Novo Nordisk, Nestlé, Rheinmetall, and many others have announced significant investments in expanding production capacity in Europe for 2025. Cheaper labour costs have favoured nearshore production in Eastern Europe.

Source: Statista, Poland Manufacturing, Hungary Manufacturing, IN Tech House

Our index approach

The VettaFi Making Europe Great Again Index (VFMEGA) tracks the market performance of companies listed globally on recognized exchanges that provide exposure to European defence, energy, infrastructure, and nearshoring spending. Additionally, a negative screen is utilized to exclude companies with exposure to controversial weapons, thermal coal, or greater than 5% exposure to tobacco.

Universe:

The universe for the defence, energy, and infrastructure segments is defined as global equities headquartered and incorporated in European countries trading on major global exchanges. The following countries are eligible: Albania, Austria, Belgium, Bulgaria, Switzerland, Cyprus, Czech Republic, Germany, Denmark, Estonia, Spain, Finland, France, United Kingdom, Greece, Croatia, Hungary, Ireland, Iceland, Italy, Lithuania, Luxembourg, Latvia, Montenegro, Netherlands, Norway, Poland, Portugal, Romania, Sweden, Slovenia, and Slovakia.

Nearshore Europe includes the following countries: Austria, Belgium, Switzerland, Cyprus, Czech Republic, Germany, Denmark, Estonia, Spain, Finland, France, United Kingdom, Ireland, Iceland, Italy, Lithuania, Luxembourg, Latvia, Netherlands, Norway, Portugal and Sweden. Benefiting countries include the following: Albania, Bulgaria, Croatia, Greece, Hungary, Montenegro, Poland, Romania, Slovakia, and Slovenia.

Constituent selection:

The top 10 companies per segment are selected based on a combined average rank of their full market capitalization rank and 3-month average daily trading value (ADTV) rank. To be eligible for inclusion, a company must meet a minimum thematic exposure to one of the specified sectors, with a special exception for companies in the nearshoring universe:

Minimum thematic exposure for defence, energy, and infrastructure segments must derive more than 50% of its revenue from one of the following segments:

Defence: Companies involved in the manufacturing and development of defence equipment (aerospace, military armoured vehicles & tanks, weapon systems and missiles, munitions and accessories, electronics & mission systems, and naval ships), or defence technology applications.

Energy: companies involved with exploration, extraction, refining, transportation, storage, distribution, or generation of energy.

Infrastructure: Companies involved with building, designing, owning, managing, or operating new or existing infrastructure.

All companies in the Nearshoring universe are eligible for inclusion.

ESG/Human rights filter:

Constituent business operations must comply with the United Nations Global Compact (UNGC) principles and Organization for Economic Cooperation (OECD) Guidelines for Multinational Enterprises. Companies involved in the production, development, or maintenance of anti-personnel mines, biological or chemical weapons, cluster munitions, or depleted uranium are excluded from consideration for the index. Additionally, companies must derive less than 5% of their revenue from tobacco manufacturing, distribution, and the sale of tobacco products, as well as not derive any revenue from the exploration, mining, or refining of thermal coal.

Additional selection criteria:

- Minimum size: Securities of companies with a market capitalization below $500 million USD are excluded.

- Minimum free-float: Securities with a free-float of less than 20% are excluded.

- Float market cap: $100 million USD.

- Minimum liquidity: Securities with a 3-month ADTV below USD 1 million are excluded.

- Maximum # names: 40 Constituents with a maximum of 10 Constituents per segment.

- Minimum 3-month trading days: 22

- Rebalanced quarterly: (Jan, Apr, Jul, Oct). Constituents are equal weighted at time of rebalance.

For more information about the VettaFi Making Europe Great Again Index (VFMEGA) click here. To capture this opportunity in an investable product, the index has been licensed in Europe by HANetf for a European UCITS ETF, the Making Europe Great Again ETF (GR8) . A non-screened version has also been licensed for an exchange-traded product in the U.S., which is expected to launch in the coming year.