VettaFi recently launched its first covered call index, the VettaFi Energy & Natural Resources Covered Call Index (NDIVY). The underlying basket of energy and natural resource equities already generates a dividend yield of around 6-7%, supported by strong cash flows. The covered call component then combines these long equity positions with monthly rolling short call options selected through a Delta-driven algorithm that targets 0.50% in monthly premium income.

-

Sustainable cash flows generating attractive dividend yields

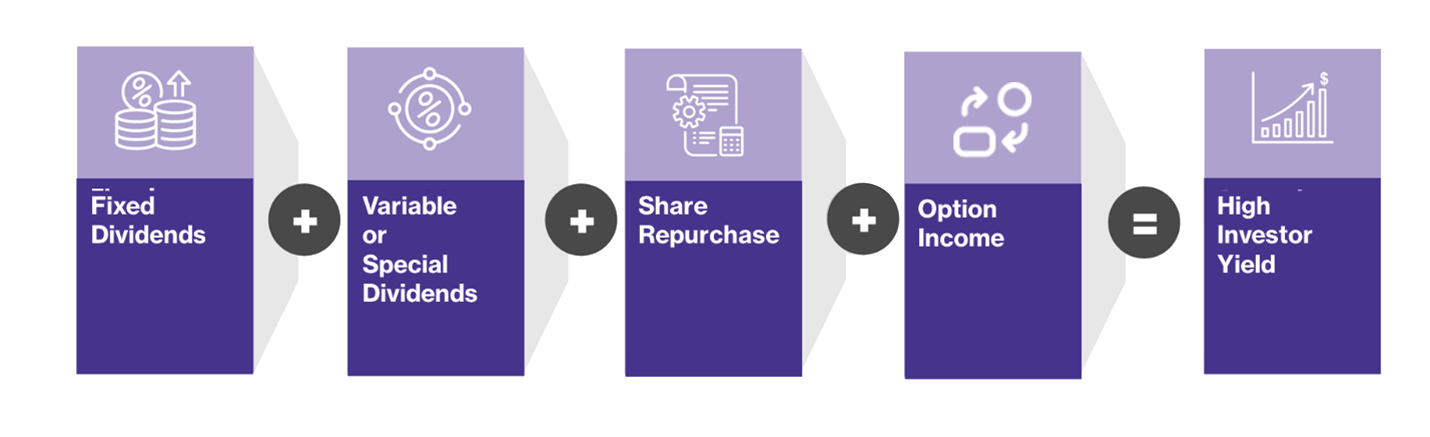

Given the lack of investment in expanding production capacity, cash flow is being returned to shareholders in the form of dividends and share repurchases. The current dividend yield for the equity portion of the index is 7%. -

Covered call overlay to enhance dividend yield

The covered call overlay targets monthly option income of 0.50%, potentially equating to 6% per year. Investors can expect an additional 3-4% of income or 10-11% income combined, supporting the “targeting 10% annual income” claim.

By mechanically writing out-of-the-money (OTM) call options, the option-based, income overlay maintains industry exposure to natural resources and energy companies, while adding as much as an additional 6% of incremental income each year.

How covered calls work

A covered call strategy is an options trading strategy implemented by a seller who owns shares in the underlying asset. Covered calls are considered a neutral strategy, meaning that the investor expects only a minor change (increase or decrease) in the share price for the life of the written call option before expiration (monthly). The investor holds the underlying assets long and simultaneously holds a short position via the option to generate additional income from the option premium. Adding a covered call option overlay enhances the distribution yield by converting equity market volatility into immediate monthly cash flows. In addition, covered calls offer short-term downside risk protection. In a sideways, choppy, or slightly declining market, collective option premiums can help as a downside buffer to bolster “long only” index returns.

Do covered call strategies need to be active?

Covered Call ETFs have become a popular investment vehicle for income-oriented investors with ~$150 billion in US assets under management, according to VettaFi estimates. While approximately 80-85% of covered call strategies are considered “active”, VettaFi’s indexed approach provides evidence that covered calls can also be implemented through a systematic, automated process as well. Utilizing inputs from its data partners, OptionMetrics and Intercontinental Exchange (ICE), VettaFi can manage the writing of call options on an underlying index or basket of stocks, including decisions on the target premium and monthly roll. And by systematically only writing call options on a portion of the underlying portfolio, market upside and industry exposures can be preserved. These rules-based decisions are then implemented by the ETF subadvisor tracking the index.

Advantages of a rule-based approach

Similar to other systematic strategies, rules-based covered call strategies eliminate the need for human intervention to “time” volatility or pick the perfect strike price manually. From an ETF issuer perspective, especially those without in-house option capabilities, indexed covered call strategies can offer a more scalable and efficient solution for yield enhancement, by facilitating consistent, repeatable investment outcomes.

Learn more about our index strategy

To read the index methodology and learn more about the index approach behind the VettaFi Energy & Natural Resources Covered Call Index (NDIVY) click here. The index is tracked in the US by the Amplify Energy & Natural Resources Covered Call ETF (NDIV).