The first quarter of 2026 was a masterclass in fixed income volatility. After a blistering start, markets pivoted toward safe haven Treasuries as geopolitical tensions drove the 10-year yield hit 4.48%. Investment-grade ETF flows reversed sharply as sentiment soured, swinging from $12 billion in February inflows to a $5 billion bleed in the final week of March.

At the same time, IG debt issuance also rang in a record first quarter, as hyperscalers became some of the largest issuers in the market. Already, the AI arms race has led Amazon, Alphabet, Meta, Microsoft and Oracle to issue roughly $100 billion to $120 billion in new debt – nearly eclipsing their 2025 totals in just three months.

Despite strong demand, the surge in supply and the spike in crude prices initially caused spreads to widen spreads before modestly firming back up. These issuers, once trading at a premium, are now trading in line with legacy industrials.

Problem with traditional indexing

This shift exposes a growing friction in fixed income benchmarks: market-cap weighting rewards the most indebted issues. The more debt they carry, the larger their footprint in your portfolio. As hyperscalers flood the market, traditional indices force investors to increase exposure just as spreads are softening.

But the rise of active management hasn’t rendered indices obsolete – it has simply raised the bar for what an index must do. Today’s investors want optimized exposure: a way to navigate a market dominated by jumbo issuers without being tethered to their issuance cycles.

Reaching for enhanced yield

This is where VettaFi’s new suite of Yield Enhancing Indices enters the fray. These two indices – which currently focus on the U.S. and European corporate credit markets – apply a disciplined, rules-based framework to extract incremental yield without falling into the traditional traps of extending duration or sacrificing liquidity.

Samarth Sanghavi, Head of Fixed Income at VettaFi, said these new indices were designed to address that very issue.

“Improving yield within [investment grade]typically involves a familiar set of tradeoffs: extending duration, accepting lower liquidity, or concentrating exposure in smaller, less widely held securities,” said Sanghavi. “The Yield Enhancing Index was built to sidestep these tradeoffs.”

Built-in guardrails

The indices generate incremental yield through a three-stage process that removes the guesswork from credit selection. The first two stages determine which issuers to hold and in what proportions, while the third optimizes how weight is allocated among specific bonds within each company’s capital structure. Collectively, this three-stage engine combines top-down macro guardrails with bottom-up bond optimization.

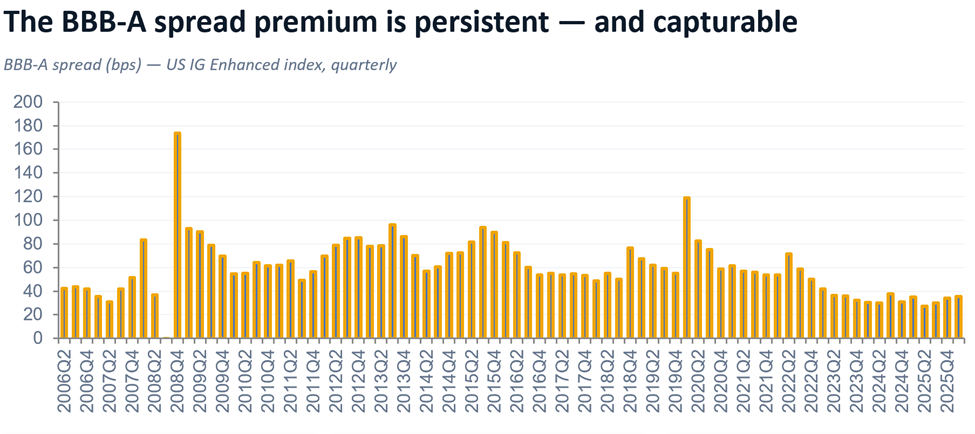

The goal is simple: capture higher income through disciplined “relative value” positioning. Specifically, the strategy is designed to lean into yield when the market is paying you to take credit risk (when BBB-A spreads are wide), and scale back in tighter regimes. By using predictable, rules-based controls, the index stays disciplined across the full credit cycle, remaining largely market-agnostic.

Source: VettaFi

The equal-weight edge: Neutralizing concentration risk

Crucially, VettaFi breaks the “debt-weight” link by equal-weighting issuers. This ensures a “debt tsunami” from a few tech giants doesn’t create unintended concentration risk. While the indices are new, the underlying strategy carries a 20-year track record of institutional-grade precision.

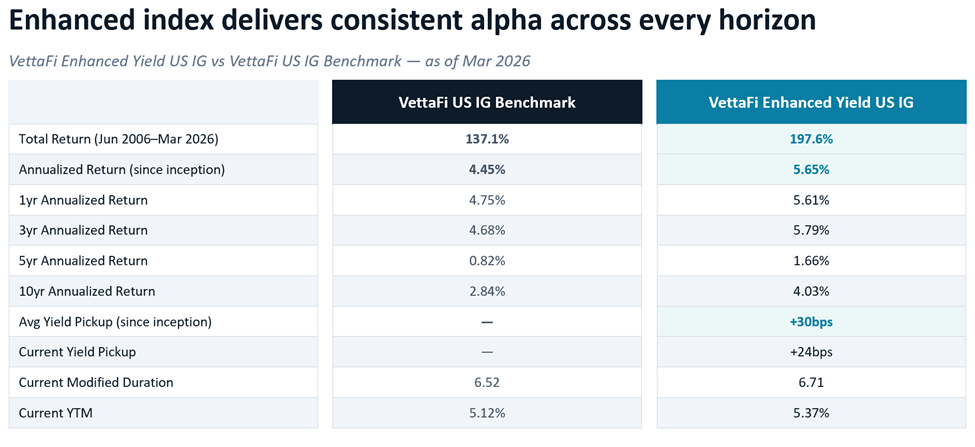

Source: VettaFi

In a year where rate spikes have dampened the total return trade, the ability to harvest a consistent 30 basis point yield advantage over the standard benchmark is no small feat. Not to mention, 70% of months have generated positive excess returns because the index relies on rules rather than emotions – rebalancing based on objective BBB-A spreads.

No hidden risks

The strategy specifically anchors the two biggest concerns for bond investors today:

- Duration: While many active managers were caught “long duration” during the March rate spike, this strategy keeps duration tightly anchored (within 0.25 years of the benchmark).

- Credit quality: A hard 65% cap on BBB exposure ensures the portfolio never drifts into “junk-lite” territory.

We are entering a clear stock picker’s market for bonds, and many index proponents would argue transparency is the new alpha. VettaFi’s indices provide “active-like” results (112 bps of annualized excess return) with the transparency and lower cost of an index. By selecting no more than 200 issuers, the index ensures low turnover and a stable core. It’s not just about picking the right company – it’s about picking the right bond within that company’s debt stack to maximize yield per unit of duration.

Believing in bond benchmarks again

Active fixed income ETFs have seen explosive growth, but momentum actually cooled in March, as investors sought the familiarity of benchmarks. Active only captured about a quarter of category flows – down from the 40% share seen in January and February. There’s no denying the massive flows into active bond ETFs, which accounted for nearly 40% of total flows early this year, but the bond index is not down and out – it’s evolving. Turns out, indices can offer their fair share of sophistication, too.

This article was originally published April 8th, 2026 on ETF Trends.