Stablecoin and its underpinning ecosystem have the potential to revolutionize the global payment system. But first, what is stablecoin? Stablecoins are tokenized cash issued on the blockchain, most commonly backed by fiat currency. It combines the stability of fiat currency or an underlying asset with the speed, security, and cost efficiency of blockchain technology. While you probably would not use Bitcoin to pay for your pizza given its volatility as a form of currency, you could pay for your pizza with stablecoin as a form of digital payment similar to using ApplePay, CashApp, or Venmo. A more common and ubiquitous use case for stablecoin than buying pizza is settling cryptocurrency trades. Given it is crypto native, stablecoin can facilitate faster and cheaper crypto settlement, allow traders to move funds more easily, support arbitrage opportunities between crypto exchanges, and provide on-ramps and off-ramps for fiat currency.

Increasingly, stablecoins are becoming a core layer in the crypto economy for digital payments, lending, and tokenization of assets. Currently issued mostly in U.S. currency, McKinsey and company reports that stablecoin circulation has doubled over the past 18 months to $300 billion from $120 billion. Stablecoin transactions are forecasted to reach more than $400 billion in value by year-end 2025, and as much as $2 trillion by 2028. Stablecoin holds the potential to challenge the incumbent cash payment rail structure and permanently disrupt it.

Tokenized money

Tokenized money is a digital representation of a financial asset on a blockchain or distributed ledger. These tokens are essentially a digital claim on an underlying asset, and their ownership is recorded and managed by smart contracts. Tokenization technology is being adopted by major financial institutions and central banks to modernize payment systems and increase scale and efficiency.

Tokenized money comes in many different forms, each with a unique issuer and underlying asset structure:

- Bank-issued tokenized deposits or deposit tokens are digital representations of commercial bank deposits issued by banks, backed one-for-one by money on the bank's balance sheet. Because they are issued by regulated institutions, they are still subject to banking regulations and deposit insurance frameworks. One example is JP Morgan’s JPM Coin.

- Central bank digital currencies (CBDCs) are digital forms of a country's fiat currency issued and backed by its central bank. A CBDC is the digital equivalent of cash and is a direct liability of the central bank similar to treasuries, making it a risk-free asset. They are designed to maintain a stable value relative to a traditional currency like the U.S. dollar by holding reserves. Examples include the People’s Bank of China’s e-CNY and the Eastern Caribbean Central Bank’s DCash (EC Dollar).

-

Stablecoins are cash-equivalent digital assets issued by a private entity, such as a licensed financial institution or a technology company. Stablecoins are designed to maintain a stable value relative to a traditional currency like the U.S. dollar and are backed by holding reserves.

Key benefits of stablecoin

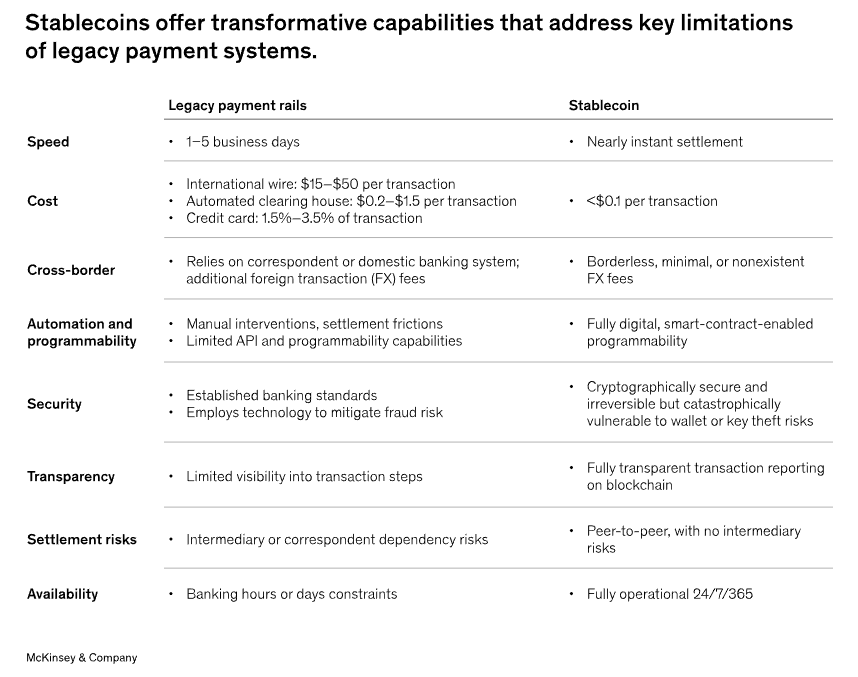

A primary goal of asset tokenization is overcoming financial fragmentation. The world is increasingly interconnected across financial and trade flows, but our current global payment infrastructure is still very slow, inefficient, and unable to scale. Stablecoin was born out of a growing need for a more efficient cash payment system than those offered by legacy payment rails.

Stablecoin-based payments are instantaneous, lower cost, have increased end-to-end traceability and visibility on-chain, and offer 24-7 on-chain liquidity. Stablecoin also provides expanded access and financial inclusion to the world’s unbanked population, given it is wallet-based rather than account-based. The benefits of stablecoin and its ecosystem are further detailed in the table below:

As a form of digital cash, consumers, merchants, and institutions can utilize the stablecoin ecosystem to transact in a variety of ways beyond just payment. Those include yield generation on savings, lending, and currency translation. Another key advantage of stablecoin for digital asset (DeFi) investors is that it keeps cash on-chain, avoiding having to toggle between the DeFi and traditional finance worlds. Today, nine out of 10 use cases for stablecoin are crypto-to-crypto transactions. However, other important potential use cases for stablecoin are becoming increasingly recognized.

Types of stablecoins

Not all stablecoins are created equal regarding the way they maintain their stable value. According to TRM Labs, more than 90% of fiat-backed stablecoins are pegged to the U.S. dollar, with Tether (USDT) and Circle (USDC) accounting for 93% of the total stablecoin market capitalization as of its latest report. But there are stablecoins tied to other asset types as well.

- Fiat-Backed Stablecoins. Fiat-backed stablecoins have a 1:1 backing by a fiat currency such as the U.S. dollar, Euro, or British Pound. For each unit of stablecoin, an equivalent amount of fiat (or its equivalent) is held in reserve by the company. The leading issuers of fiat-backed stablecoins are Tether and Circle. This model requires trust in the issuer in addition to the issuing country/economic union of the pegged currency.

- Crypto-Backed Stablecoins. Crypto-backed stablecoins are backed by cryptocurrencies such as Bitcoin or Ethereum. They are often over-collaterized to offset daily volatility.

- Algorithmic Stablecoins. Algorithmic stablecoins utilize smart contracts to control supply and demand to maintain a stable value without relying on collateral. These stablecoins carry higher risk as they are subject to de-pegging in times of high volatility.

-

Commodity-Backed Stablecoins. Commodity-backed stablecoins are pegged to tangible commodities such as gold, silver, diamonds, and oil, offering a hedge against inflation and market volatility. Market fluctuations in the underlying asset can impact the stablecoin value. If this investment construct sounds familiar, it is basically equivalent to an on-chain version of a physical commodity ETF.

Stablecoins in circulation

The top ten stablecoin tokens by market capitalization, as of October 24, 2025, are:

Tether (USDT). The first stablecoin, dating back to 2014, remains the most widely-used in the crypto space by trading volume. Pegged to the U.S. dollar, it is commonly used to provide liquidity for trades and DeFi activities. Tether’s market share leads with 58% of the market.

Tether (USDT). The first stablecoin, dating back to 2014, remains the most widely-used in the crypto space by trading volume. Pegged to the U.S. dollar, it is commonly used to provide liquidity for trades and DeFi activities. Tether’s market share leads with 58% of the market.  USDC (USDC). Initially issued by Circle and Coinbase under a consortium (now just Circle), it is backed 1:1 by the U.S. dollar. It was created in 2018.

USDC (USDC). Initially issued by Circle and Coinbase under a consortium (now just Circle), it is backed 1:1 by the U.S. dollar. It was created in 2018.  Ethena USDe (USDe). Considered a next generation stablecoin, it mixes a hybrid design of crypto and algorithmic smart contracts to provide stability. It was created in 2023.

Ethena USDe (USDe). Considered a next generation stablecoin, it mixes a hybrid design of crypto and algorithmic smart contracts to provide stability. It was created in 2023.  Dai (DAI). A decentralized stablecoin governed by MakerDAO (DAO). Unlike fiat-backed stablecoin, DAI is backed by a mix of cryptocurrencies. Its algorithm adjusts collateral requirements to maintain its 1:1 peg to the U.S. dollar. Dai is a cornerstone of the DeFi ecosystem, powering lending, borrowing, and yield farming applications in the MarketDAO ecosystem. DAI was created in 2017.

Dai (DAI). A decentralized stablecoin governed by MakerDAO (DAO). Unlike fiat-backed stablecoin, DAI is backed by a mix of cryptocurrencies. Its algorithm adjusts collateral requirements to maintain its 1:1 peg to the U.S. dollar. Dai is a cornerstone of the DeFi ecosystem, powering lending, borrowing, and yield farming applications in the MarketDAO ecosystem. DAI was created in 2017. PayPal USD (PYUSD). PayPal has entered the stablecoin market with a token built on top of its global payment network. Its stablecoin is fully backed by USD reserves and cash equivalents. PYUSD hopes to bridge the gap between traditional finance and the blockchain and is designed for retail and institutional use with applications for ecommerce, Web3 integration, and payments.

PayPal USD (PYUSD). PayPal has entered the stablecoin market with a token built on top of its global payment network. Its stablecoin is fully backed by USD reserves and cash equivalents. PYUSD hopes to bridge the gap between traditional finance and the blockchain and is designed for retail and institutional use with applications for ecommerce, Web3 integration, and payments.  World LIbery Financial (USD1). This fiat-based digital asset is designed to maintain a stable value relative to USD, backed by U.S. dollars and other liquid assets. It was launched in April 2025 by World Liberty Financial.

World LIbery Financial (USD1). This fiat-based digital asset is designed to maintain a stable value relative to USD, backed by U.S. dollars and other liquid assets. It was launched in April 2025 by World Liberty Financial.  Falcon (USDf). A synthetic stablecoin developed by Falcon Finance, representing overcollateralized digital dollars that aim to combine security, flexibility, and sustainability in their design. USDf is not pegged to fiat by direct reserves but is minted against a diversified set of collateral assets.

Falcon (USDf). A synthetic stablecoin developed by Falcon Finance, representing overcollateralized digital dollars that aim to combine security, flexibility, and sustainability in their design. USDf is not pegged to fiat by direct reserves but is minted against a diversified set of collateral assets. Global Dollar (USDG). U.S. dollar-pegged stablecoin issued by Paxos Digital in Singapore. USDG was launched November 1, 2024 by Paxos as the core asset of its Global Dollar Network. USDG is designed to function across multiple blockchains and is used by a growing ecosystem of financial and crypto institutions including Kraken, Robinhood, Mastercard and Anchorage Digital.

Global Dollar (USDG). U.S. dollar-pegged stablecoin issued by Paxos Digital in Singapore. USDG was launched November 1, 2024 by Paxos as the core asset of its Global Dollar Network. USDG is designed to function across multiple blockchains and is used by a growing ecosystem of financial and crypto institutions including Kraken, Robinhood, Mastercard and Anchorage Digital.  Ripple USD (RLUSD). Ripple’s fiat-backed stablecoin was launched in 2024 and built on its Ripple blockchain payment network to facilitate low-cost global transfers. LIke the XRP token, Ripple is optimized for cross-border transactions and well suited for institutional customers.

Ripple USD (RLUSD). Ripple’s fiat-backed stablecoin was launched in 2024 and built on its Ripple blockchain payment network to facilitate low-cost global transfers. LIke the XRP token, Ripple is optimized for cross-border transactions and well suited for institutional customers.  USDD (USDD). This stablecoin was created by the TRON DAO Reserve which aims to maintain its 1:1 peg with USD using a system of overcollateralized crypto assets and a peg stability module (PSM) to help maintain its value. USDD was launched in 2022, amid the collapse of algorithmic stablecoin UST.

USDD (USDD). This stablecoin was created by the TRON DAO Reserve which aims to maintain its 1:1 peg with USD using a system of overcollateralized crypto assets and a peg stability module (PSM) to help maintain its value. USDD was launched in 2022, amid the collapse of algorithmic stablecoin UST.

Source: CoinMarketCap, MoonPay

The GENIUS Act and stablecoin regulation

The GENIUS Act (Guaranteeing Essential National Infrastructure in U.S. Stablecoins) was passed on July 17, 2025. It creates a new U.S. regulatory framework for payment stablecoin issuers to operate in the U.S. and for foreign entities to offer stablecoins to U.S. residents. It represents the first major cryptocurrency legislation passed by Congress.

The GENIUS Act addresses three major stablecoin concerns:

- Financial stability. It requires payment issuers to hold high-quality reserve assets safeguarded by qualified custodians, along with monthly reserve disclosures and published redemption policies. The Act also includes bankruptcy provisions to ensure stablecoin holders have priority claims on reserve assets.

- Cross border parity. Foreign issuers are subject to the same rules as U.S. issuers with regard to anti money laundering (AML) and sanction compliance provisions.

- Regulatory clarity. The act establishes a coherent regulatory framework for the stablecoin market in the U.S. in order to facilitate the enhanced adoption of digital assets and growth of the digital asset ecosystem. The framework also aims to attract stablecoin activity to the U.S. and increase demand for U.S. Treasuries.

Stablecoin regulation is also being implemented in other jurisdictions around the world. In December of 2024, the EU’s Markets in Crypto-Assets Regulation, (MiCA) was implemented. While it does not refer specifically to stablecoins, it does address e-money tokens (EMT) backed by fiat currency. Under MiCA, only regulated e-money institutions or credit institutions can issue EMTs. Additionally, Hong Kong passed a Stablecoin Ordinance in May of 2025. Under the law, all issuers of stablecoins backed by the Hong Kong dollar will need to obtain a license issued by the Hong Kong Monetary Authority. Stablecoins must be backed by high-quality, liquid reserve assets, and the market value of the reserve pool must be equivalent to the par value of the stablecoins circulated. Stablecoin issuers are also subject to strict regulatory requirements, including AML and CFT laws and regular audits and disclosure.

The passage of the GENIUS Act has paved the way for further institutional adoption and further expansion of the stablecoin ecosystem. JP Morgan predicts that “the Genius Act could further accelerate stablecoin adoption, moving this asset class more mainstream and further fueling the growth of this market.” The GENIUS Act creates a state and federal regulatory pathway to add new players to the stablecoin ecosystem, including non-banks, subsidiaries of insured depository institutions and state-chartered entities. However, these issuers will be prohibited from offering yield or interest, so as not to compete with interest-bearing bank and money market deposits.

According to a new report from TRM Labs, stablecoins now comprise 30% of all on-chain crypto transaction volume, exceeding more than $4 trillion for the year, and representing an 83% increase over the same period in 2024.

Already, passage of the GENIUS Act and Solana ETFs have accelerated Solana's stablecoin growth over the last three months by 40%, outpacing Ethereum's 27% expansion over the same period. Circle's USDC dominates 77.4% of Solana's stablecoin market. While Ethereum still maintains a 60% share of the stablecoin market, versus Solana’s smaller 4.5% share, Solana is increasingly becoming a hub for on-chain activity, with faster throughput and cheap fees.

Growth projections for stablecoin

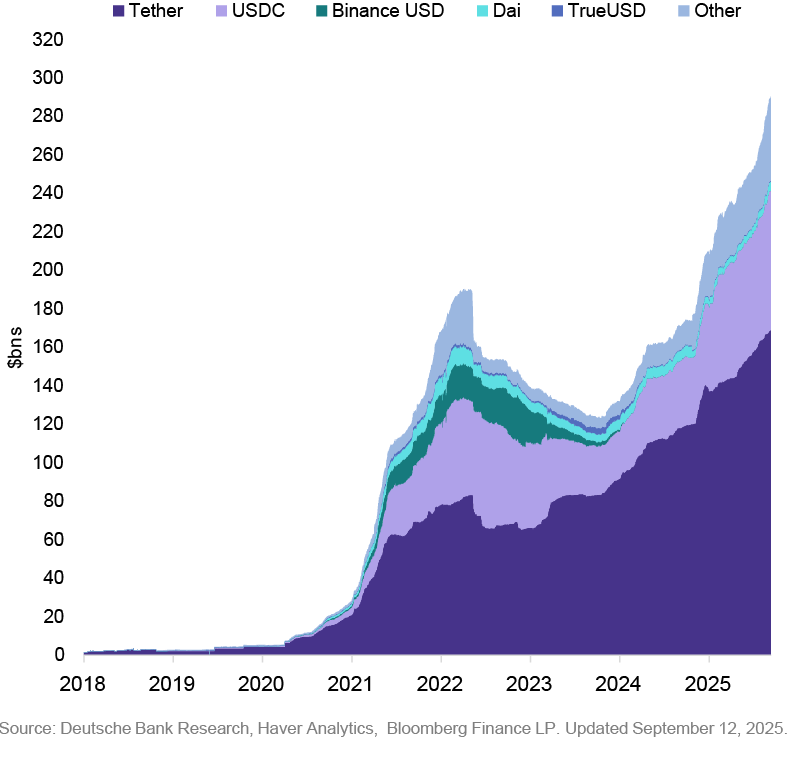

As seen in the chart below, the market capitalization for stablecoin surged from $5 billion in 2020 to $290 billion in September 2025, with initial estimates projecting a rise to $310 billion at the end of the year.

Market cap surged from $5bn (2020) to $290bn (Sep 2025)

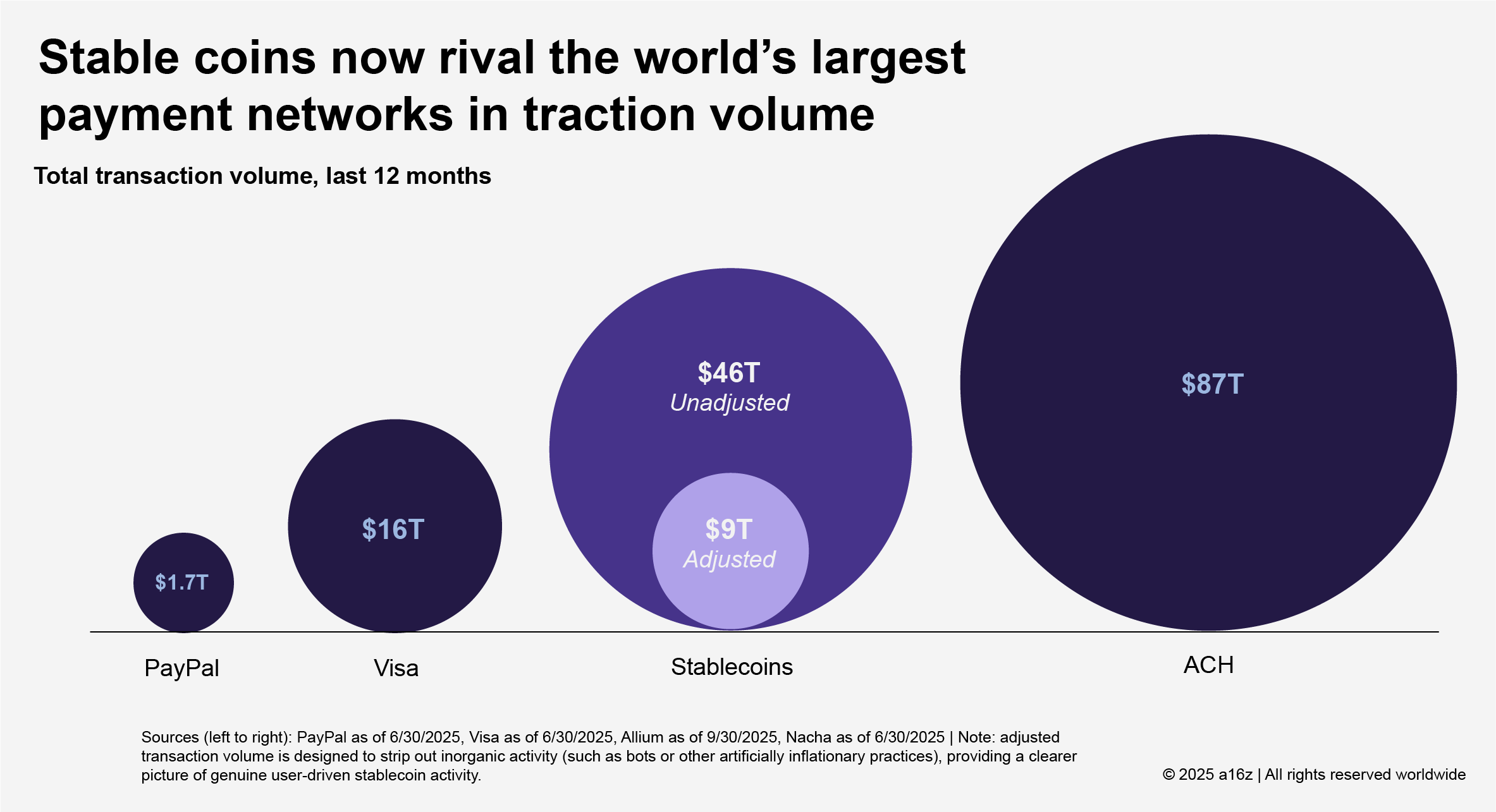

Stablecoin now rivals some of the largest payment networks in terms of transaction volume, and adoption is accelerating. According to the latest Artemis Analytics data, global stablecoin transaction volumes soared 72% in 2025, hitting $33 trillion, recording $11 trillion in transactions in just the fourth quarter alone.

While projections for the overall stablecoin market growth vary, analysis consensus is forecasting growth of between $2 and $4 trillion by 2030, with the U.S. Treasury projecting $2 trillion by 2028.

Here are some other top growth projections for stablecoin:

-

Coinbase: Projects $1.2 trillion by the end of 2028.

-

Standard Chartered: Projects $2 trillion by 2028.

-

Citi: Projects $2 trillion by 2028 and up to $4 trillion by 2030.

-

Deutsche Bank Research: Projects $2 trillion by 2028.

-

J.P. Morgan: Believes $2 trillion by 2028 is "optimistic" and projects a range of $500–$750 billion in the coming years, citing undeveloped infrastructure.

The eventual accuracy of these projections will depend on the pace of institutional adoption, regulatory outcomes, and the ability to integrate stablecoin and next-gen payments into the traditional global financial ecosystem. Major payment enterprises and traditional finance entities are fast realizing the need to become part of the stablecoin ecosystem.

The future of stablecoin

What does the future hold for stablecoin? Here is a brief glimpse:

-

Banks will be issuing their own stablecoins;

-

Stablecoin issuers like Circle will launch payment networks;

-

Ecommerce giants Amazon and WalMart will issue stablecoins;

-

Ecommerce platforms like Shopify will offer plug-ins for seamless crypto payment;

-

Money transfer platforms like Zelle will integrate stablecoin functionality;

-

Financial technology leaders like Stripe will enhance their payment rails via strategic acquisitions like its $1.1 billion acquisition of Bridge;

How can investors get access to the growth potential of the stablecoin ecosystem?

Our index approach

The VettaFi ROBO Stablecoin Ecosystem Index (PEGG) is an index of global companies that tracks companies strategically positioned to enable the development, adoption, and operation of stablecoins across the digital asset landscape, including those involved in issuance, custody, reserve management, infrastructure, and payment solutions.

For more information about the VettaFi ROBO Stablecoin Ecosystem Index (PEGG), click here. The index has been licensed by Grayscale for the Grayscale Stablecoin Ecosystem ETF (PEGG), expected to launch in February 2026.