Drones, also known as unmanned aerial vehicles (UAVs), are commonly used today for many enterprise applications and use cases across different sectors and industries such as defense, security, energy, construction/infrastructure, agriculture, logistics, utilities, real estate, photography/filming, and insurance. Private consumers even use drones today recreationally and for entertainment such as drone shows. Regardless of the end consumer, the modern appeal of drones lies in their low cost, utility, portability, and technology features integrating drone hardware, cameras, and sensors with software, data integration capabilities, mapping, and even artificial intelligence (AI).

History of drones

Interestingly, drones are not new; they have been around for almost a century. The first drones were remote-controlled wooden airplanes that the British Navy used for target practice in the 1930s. Over the years, the military has provided most of the funding behind drone research and applications. Private interest in drones did not pick up until the early 2000s, when declining costs for electronic components, advancements in connectivity, and innovations in lithium battery technology made consumer drones economically viable. While consumer drones are designed to be small, inexpensive, and nimble, enterprise drones have also evolved into an economical source of unmanned air power and a tool for data collection.

Investment case for drones

Pardon the pun, but the drone market is taking off. The drone industry’s rapid ascent is being fueled by the growing number of commercial and military applications, along with a more supportive regulatory environment.

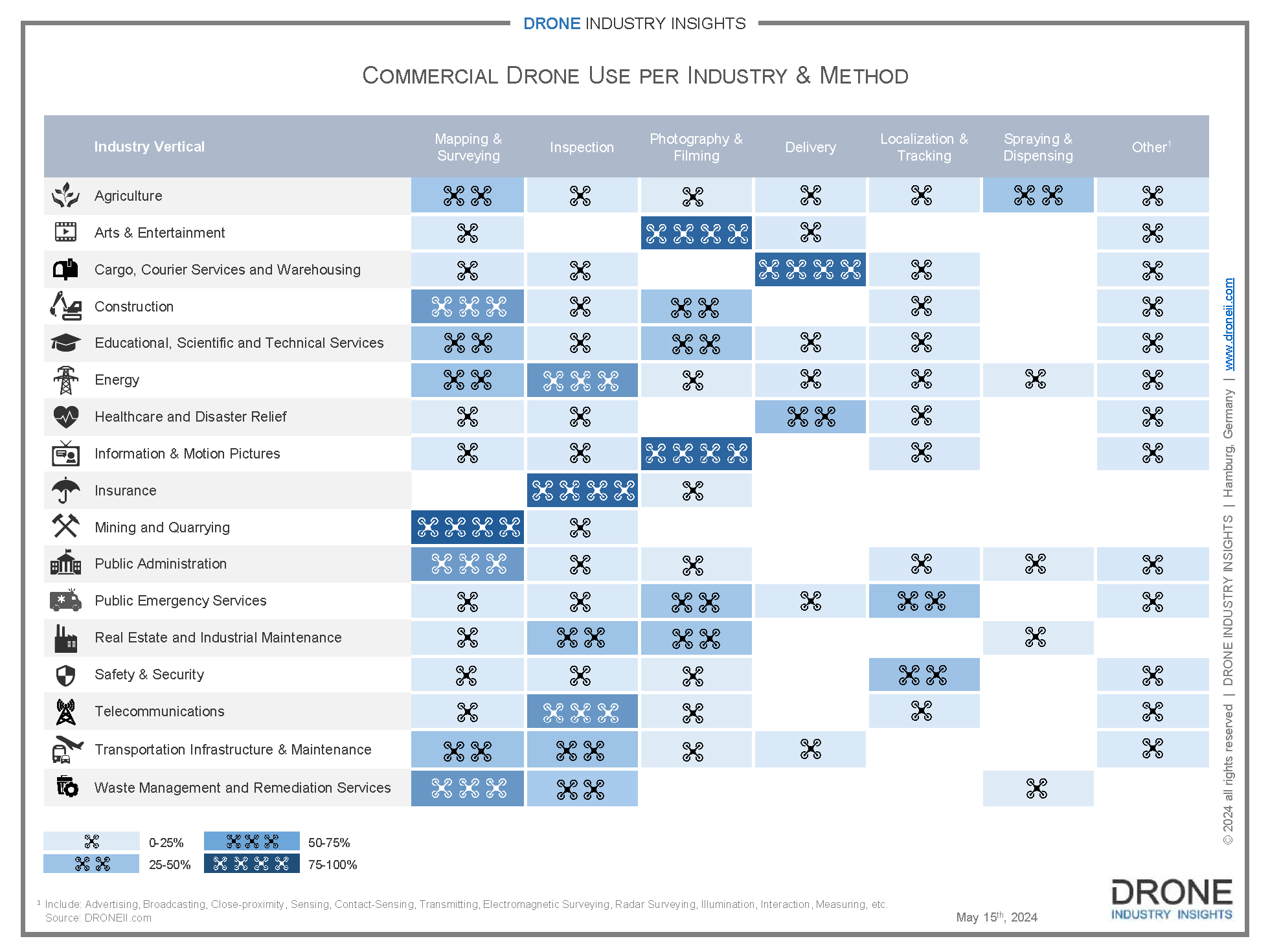

Commercial applications & use cases

Drone technology is now used for a wide range of commercial tasks. According to Dronell’s 2024 Drone Industry Insights report on commercial drone use, the top industries for drone applications are energy, construction, and agriculture, with the top applications being drone mapping & surveying, drone inspections, and drone photography and filming. The graphic below highlights the fact that every major industry in the world is now using drones thanks to innovation in sensor technology, software, connectivity, and battery life. The global commercial drone market is expected to grow to $57.8 billion by 2030, achieving a compound annual growth rate of 8%. Flexibility is another key element leading to the rise of commercial drone adoption. Drones come in a variety of price points, shapes, sizes, and weights. They can adapt payloads and sensors aligned with specific needs and financial resources.

Increased military adoption

In a world of rising global instability, drone technology is playing a pivotal role as a military asset. Military drones are used for intelligence, surveillance, reconnaissance (ISR) and targeting, facilitating precision strikes with situational awareness. Military drones are equipped with sensors such as high-resolution cameras, infrared and thermal sensors that can identify targets and threats. These drones also use advanced communication systems such as satellite and secure data transmission methods like Li-Fi (wireless communication using light transmission). And today’s military drones also integrate AI and machine learning to enhance autonomy and improve the accuracy of decision making.

Some of the key use cases for military drones include:

-

Intelligence, surveillance, reconnaissance (ISR) - Drones equipped with advanced sensors, cameras, and satellite imaging monitor enemy movements, map terrain, and relay this information to troops on the ground.

-

Precision strikes - Armed drones or unmanned combat aerial vehicles (UCAVs), armed with missiles to attack targets identified during ISR.

-

Logistics - Drones can be used to deliver supplies and equipment efficiently to difficult-to-reach areas.

-

Counter drones - Drones can be used to jam or disrupt enemy communications and systems.

-

Simulation - Drones can be used to simulate real-life enemy aircraft and missile scenarios.

-

Secure communication relay - Drones can serve as mobile communication nodes to securely relay information among battlefield units.

-

Force & special ops protection - By providing continuous, real-time surveillance information from a high altitude, drones can help protect troops and support special operations.

-

Drone swarms - Increasingly, drones are being used in “swarm” configurations, with coordinated groups of autonomous drones being used together for tasks such as surveillance or an armed attack.

-

Interceptor drones & nets - Interceptor drones can be equipped with “nets” to physically capture or collide with hostile drones. Other countermeasures to drones and drone swarms include jammers and lasers designed to neutralize them individually and en masse.

Drones have become a game changer for 21st-century military strategy. The modern military favors using drones given their ability to reduce the loss of human life, provide a cost-effective alternative to expensive military aircraft, and provide operational flexibility unmatched by manned aircraft solutions. All of this has played out in real-time during the Russia/Ukraine war, which has amplified the utility of having small, maneuverable, and adaptable air systems that reduce the risk to military personnel. As we have seen first-hand in that military battle, a $700 drone can knock out a multimillion-dollar tank. Drones are relatively inexpensive, small (making them harder to detect), able to inflict significant damage, and capable of posing a disproportionate threat. Drone technology can be used defensively as well. Europe is currently considering implementing a “drone wall” to counter recent acts of hybrid Russian aggression. A “drone wall” is not a physical wall; it layers a network of detection and interception systems building on already-existing anti-drone capabilities.

It is no wonder that the global market for military drones is growing rapidly. It is expected to reach $88 billion by 2030, with a compound annual growth rate of 14%, propelled by increasing military budgets. This growth is being driven by rising geopolitical tensions, increased military budgets aiming for greater cost efficiency and flexibility, and technical advancements in drone technology, including AI-powered surveillance and autonomous capabilities.

Some of the largest military drone manufacturers include U.S. companies such as General Atomics, Lockheed Martin, Northrop Grumman, AeroVironment, and Kratos Systems; Turkey’s Baykar Technologies; and Israel’s Elbit Systems. The table below provides a list of top military drone platforms and their strengths.

Top military drone manufacturers (2025)

|

Company |

Country |

Key Platforms |

Strength |

|

General Atomics |

U.S. |

MQ-9 Reaper, Predator |

Long endurance strike & ISR |

|

Lockheed Martin |

U.S. |

Stalker, Desert Hawk |

Cutting-edge autonomy & VTOL |

|

Northrop Grumman |

U.S. |

Global Hawk, Triton |

High-altitude, maritime ISR |

|

Baykar |

Turkey |

TB2, Akinci |

Export-ready combat drones |

|

Elbit Systems |

Israel |

Hermes 450/900 |

Advanced ISR tech & sensors |

|

IAI |

Israel |

Heron, Harop |

Loitering munitions & ISR |

|

AeroVironment |

U.S. |

Raven, Puma, Switchblade |

Small tactical drones |

|

Kratos |

U.S. |

XQ-58 Valkyrie |

Loitering loyal wingman |

|

Anduril Industries |

U.S. |

Fury, Ghost |

AI-loaded autonomous UAVs |

|

Hinaray Technology |

China |

HN-VF55P, HP100/200 |

VTOL/hybrid & counter-drone systems |

Source: Hinaray Technology

Changing regulations

The U.S. Department of Transportation has proposed a sweeping new rule that would finally normalize beyond visual line of sight (BVLOS) drone operations. This long-awaited milestone for the commercial drone industry, introduced as Part 108, is being hailed as a transformative framework that will allow drones to operate beyond the operator’s visual range without the need for individual waivers. At the global level, International Civil Aviation Organization (ICAO) Council Unmanned Aviation and Advanced Air Mobility standards are also being updated and reformed to address remote pilot systems.

Our index approach

The VettaFi Drone Index (DRONES) is an index comprising global companies that provide exposure to drones and unmanned aerial vehicles (UAVS). The index contains companies that are engaged in drone/UAV manufacturing and enabling technologies.

To be eligible for inclusion in the index, constituents must have a minimum thematic exposure as follows:

-

Constituent business operations must derive more than 20% of their revenues from drones/UAVs or enabling technologies, or

-

Constituents must be a defense company with a division/program designated for R&D of drones/UAVs.

At time of quarterly rebalance, companies must have a market capitalization of at least $100 million USD or $75 million for current constituents, a 15% free float, and a three-month average daily traded value of $500,000 USD, or $400,000 USD for current constituents.

The Index uses a modified free-float market-capitalization-weighted algorithm with companies weighted either within a pure-play or diversified tranche.

Pure-play companies must derive at least 50% of their revenue from drones/UAV manufacturing or enabling technology. Diversified companies must derive at least 20% of their revenue from drones/UAV manufacturing or enabling technology; or be a defense company with a division/program designated for R&D of drones/UAVs. Eighty percent of the index is in the pure-play weighting scheme to ensure meaningful drone industry exposure.

For more information about the VettaFi Drone Index (DRONES), click here. The index has been licensed by RexShares for the Rex Drone ETF (DRNZ), which is expected to launch in October.