The Indo-Pacific region includes the countries of Australia, India, Indonesia, Japan, New Zealand, the Philippines, Singapore, South Korea, Taiwan, and Thailand. The region has become an area of rising strategic importance, due to China’s global military expansion, ongoing tensions in the South China Sea related to uncertainty about Taiwan, and most recently an escalation of tensions between India and Pakistan.

The uncertain environment in the region has created a sustained increase in defence spending and heightened demand for advanced, future-of-defence, military capabilities. NATO, the United States, and its allies have identified the Indo-Pacific region as a top defence priority. This has translated into record-high defence budgets, new joint cooperation frameworks such as AUKUS, the U.S.-Japan (USJF) Alliance, and the U.S.-India TRUST, and a renewed focus on technological innovation and capacity expansion.

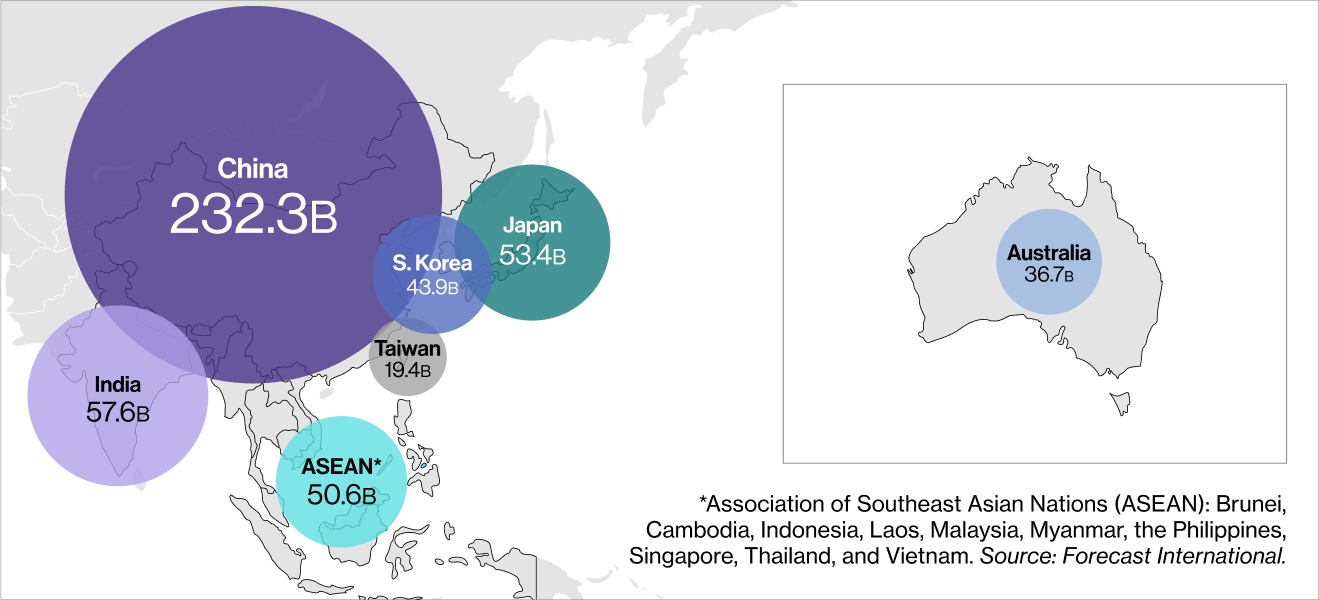

The Indo-Pacific defence market represented 22% of the world’s total global defence expenditures in 2024. China’s defence spending amounts to 46% of the region’s total, followed by India, Japan, and Taiwan, combining for a total of 26%.

2024 Defence spending by country ($USD)

While currently 65–70% of its military inventory is foreign-sourced, increasingly, countries such as Japan, Singapore, South Korea, Taiwan, and India are becoming more self-sufficient from an equipment perspective, with the potential to equip other countries in the region. Defence industrial bases of smaller, but growing, capability are also being cultivated in Australia, Indonesia, Malaysia, Thailand and Vietnam. Ultimately, similar to Europe, the future of Indo-Pacific defence is expected to become a region less dependent on foreign-sourced technologies and equipment, with the potential to partner and supply other nations on a surplus basis.

The investment case

The case for Indo-Pacific Defence exposure is as follows:

-

Rising tensions in the region - Rising geopolitical tensions and perceived threats from China, North Korea, and regional disputes are fueling record defence spending in the region.

-

Desire for regional autonomy - Push for expanded regional production and innovation along with reduced foreign dependency.

-

Strategic importance driving investment - Policy and budgetary support from NATO, the U.S., and allies given the region’s strategic importance.

A growing military presence of the U.S. and China in the region, alongside other regional powers, is fueling demand for “future of defence†advanced weaponry and defence systems. All of this means, there is more defence and defence technology spending to come, creating growth opportunities for defence and cyber defence companies in the region. According to Forecast International, growth in the Indo-Pacific defence market is expected to reach $534 billion in 2025, with growth to $644 billion by 2030.

Our index approach

The VettaFi Future of Defence Indo-Pac ex China Index tracks the performance of companies from the Indo-Pacific region ex China that generate revenues from defence and cyber defence spending.

In order to be eligible for inclusion, companies must meet the following requirements:

-

Constituent business operations must derive more than 20% of their revenues from the manufacture and development of defence equipment (military armored vehicles and tanks, weapon systems and missiles, munitions and accessories, electronics and mission systems, and naval ships), defence technology applications, or cyber security and contract with an included country verified by publicly available contract information.

-

Companies developing naval ships with less than 20% defense related revenue may be added if their defense related revenue is at least $3 billion USD.

ESG/human rights filter: Constituent business operations must comply with United Nation Global Compact (UNGC) principles and Organization for Economic Cooperation (OECD) Guidelines for Multinational Enterprises.

Controversial weapons filter: Constituent business operations must derive less than 20% of their revenue from controversial weapons.

Weighting: Constituents are modified free float-market cap-weighted. The Index is reconstituted and rebalanced on a quarterly basis on the fourth Tuesday in January, April, July, and October.

VettaFi’s Future of Defence Indo-Pac ex China Index (IPDEF) has been licensed in Europe by HAN ETFs for an exchange traded product expected to launch in July 2025. For more information about the Index, click here.